A wave of Chinese investment has led to a slew of properties and developments mushrooming in the Cambodian costal village of Sihanoukville over the last few years.

However, the Cambodian government’s recent ban on online gambling over concerns of money laundering has dealt a serious blow to the city’s tourism and real estate sector, and disrupted a three-year booming business in the country which catered primarily to Chinese tourists.

Sihanoukville retains potential for growth on the back of ongoing construction projects and development of SSEZ: C9

Still, the outlook is not entirely bleak, in light of ongoing infrastructure projects and the development of the Chinese-invested Sihanoukville Special Economic Zone (SSEZ), noted C9 Hotelworks’ Sihanoukville Tourism & Property Market Update 2020.

“Sihanoukville was originally a peaceful coastal village set in the southwest of Cambodia. In the past, it attracted mostly Western tourists and was once a weekend getaway destination for locals. However, starting in 2017, the dramatic inflow of Chinese investment driven by the Belt and Road Initiative has changed the seaside town completely,” Bill Barnett, managing director, C9 Hotelworks, said.

“Prior to 2016, only limited domestic and charter flights served Sihanoukville airport. The emerging market has drawn attention from various segments, especially the gambling sector, and brought hundreds of thousands of mainland Chinese workers and investors to the city.”

As of year-to-date October 2019, the city’s main getaway Sihanoukville International Airport hosted 602,755 passenger arrivals, which is a 266 per cent year-on-year growth compared to the same period in 2018.

Currently, the Sihanoukville airport has direct connectivity to four countries, serving 27 destinations and 22 cities in mainland China.

“Land values, rents and condominium sales prices have skyrocketed during a three-year period due to the surging demand and massive development of the city,” Barnett added.

There are currently 3,296 hotel keys in Sihanoukville, ranging from midscale to the upper upscale tier, with most properties boasting large room stock that caters to groups, said the report.

“Without a doubt, the Cambodian ban of online gambling, driven by the Chinese government has hit the tourism and real estate sector hard. Yet, ongoing construction of public infrastructure and development of SSEZ will likely contribute to stabilising development in the medium to long term,” Barnett said.

Sihanoukville International Airport is undergoing an extension of the runway to serve larger aircraft, with the project expected to be completed this year.

Despite the challenged online gambling sector, future growth is expected to be diversified in various segments, with a focus on the industrial industry alongside a rebound in tourism, said the report.

While there is massive construction of buildings in the city, key projects total 18 developments, representing 30,549 condominium units. All upcoming projects include condominiums; with six mixed-use properties also having hotels, shopping malls and office buildings.

Today’s independent hoteliers have a greater awareness and appetite around technology when it comes to their marketing and distribution strategies, noted new research backed by hotel guest acquisition platform SiteMinder.

According to eHotelier’s Marketing & Distribution 2020 Journal, 68.4 per cent of independent hotels already have a digital marketing strategy implemented for their business, while a further 24.4 per cent intend to implement their strategy over the coming year.

Number of independent hoteliers leveraging technology to drive business on the rise: study

Only 7.2 per cent of independent hoteliers do not understand the relevance of a digital marketing strategy or how it can help their hotel business, found the study which surveyed 461 hotel industry professionals from around the world, with 80 per cent from independent hotels.

James Bishop, senior director of global demand partnerships at SiteMinder, said: “These figures seemed almost unimaginable as recently as 13 years ago, when SiteMinder first opened its doors to hoteliers all around the world who yearned for a way to market and sell their rooms online.”

When it comes to the value of booking channels in driving revenue, direct website bookings remain perceived among respondents as the most important booking channel for independent hoteliers, with 62.1 per cent ranking direct website bookings as either very valuable or valuable – a sentiment accentuated among hotel chains and franchises (87.9 per cent).

Owned channels, such as direct mail and a hotel’s website, trumped paid channels, such as paid social media, in terms of their perceived effectiveness in driving business.

The study also underlined a growing desire for hoteliers to better know their customers, with direct feedback seen as the most important channel in defining how they approach their marketing strategy.

“Unsurprisingly, direct website bookings remain perceived as the most important channel, a heartening outcome for the health of the market, as it displays the enthusiasm that hoteliers of all sizes currently have to embrace the tools and innovations at their disposal. However, hotels should also remember that having a balanced distribution strategy between channels, such as OTAs, wholesalers and GDS – as well as direct – remains key in the success of marketing your hotel online,” Bishop said.

“At SiteMinder, we are encouraged to also see hoteliers looking at the distribution of data from their core platform to other applications, such as CRM, upselling tools and guest messaging, to support their overall strategy in 2020 and beyond.”

Japanese social entrepreneur Seiya Ashikari is using tourism as a tool to push Cambodia’s cricket farming industry.

In August 2018, the 24-year-old pressed pause mid-way through pursuing a biology PhD in Tokyo to volunteer on a cricket farming project in Cambodia.

Ashikari saw that growing the insects were a potential way to boost the income of farmers struggling to make ends meet cultivating traditional crops. He launched Ecologgie, helping train farmers and turn their produce into cricket-based protein powder and nutritious snacks.

The insects, which are easy to farm from the rural homes that dot the country and sold for about US$3/kg, are packed with protein – a missing ingredient from many local diets.

Now, Ashikari has launched one- and two-day cricket farming tours in Kampong Thom. The rural province is famed for its cricket farming and home to one of Ecologgie’s current two centres. The other is in Takeo.

Ashikari said: “I want visitors to learn about the cricket farming industry, and raise understanding about insects as a sustainable source of food protein in the future.”

In line with his philosophy of placing locals at the heart of his work, Ashikari’s tours are community-driven. While visitors get to see Ecologgie’s operations, grassroots cricket farmers also introduce guests to their work. Overnight guests stay with farmers in their home.

During trips into surrounding countryside, guests can see the critters in the wild. There is also the chance to accompany tarantula hunters as they head into the jungle in search of spiders.

They are caught using home-made, pronged sticks poked into spider holes. After coaxing out the arachnids, they are caught by hand, defanged and sold. Vendors then deep-fry them in garlic and chili, and sell them as tasty snacks.

Added Ashikari: “This is a great experience for people wanting to really learn about and experience local livelihoods in Cambodia. I wanted to create something different, while helping local communities.”

In 2019, Ashikari ran two tours. This year, he plans to push it as an add-on to Siem Reap trips, or to break up over-land travel between Siem Reap and Phnom Penh.

For details, contact seiya-ashikari@ecologgie.com.

Ongoing bushfires that have ravaged large parts of Australia have greatly affected Sydney Drive Regional, a submarket within a two-hour-drive radius of Greater Sydney, according to STR’s preliminary data.

For the month of December, the submarket showed a 14.7% year-over-year decline in demand (room nights sold) and subsequent double-digit declines in each of the three key performance metrics: occupancy decreased -14.5% to 52.2%, while average daily rate (ADR) fell -18.4% to A$194.74 (US$143.14) and revenue per available room dropped -30.3% to A$101.48.

New South Wales hotels suffer a dip from bushfires

“Because the physical impact of the bushfires has been predominantly across the Great Dividing Range of New South Wales and Victoria, we’ve not yet seen significant demand decreases in the major city areas of Australia,” said Matthew Burke, STR’s regional manager – Pacific.

“However, these regional locations are popular tourist spots for family holidays in vacation homes, hotels and holiday parks. The post-Christmas period to the end of January is peak season, when so many local businesses rely on the transient tourist trade. Moreover, with road closures through January, we will watch to see the impact more broadly.”

Across New South Wales, results have been mixed. The NSW North Coast submarket, or Northern Rivers region, saw a 7.0% jump in demand and a 5.8% lift in ADR, while the NSW North Coast South submarket (known as the Mid North Coast) saw muted demand growth (+0.4%).

Separately in South Australia, the impact of bushfires on Kangaroo Island has been heavy, including the destruction and significant damage to a number of properties, which will have a direct impact on tourism in the short term, said STR in a statement.

As Vietnam’s domestic tourism market continues its upwards trajectory, one local start-up is aiming to solidify the country’s fragmented industry.

Avid traveller Trịnh Dình Minh has relished visiting new destinations across his homeland while pursuing an engineering and IT degree. Trinh and his friends would visit then less-known areas, such as the northern mountainous provinces of Ha Giang, Moc Chau and Bac Kan.

Trịnh created Tago.vn to create a more seamless experience for travellers

Said Trinh: “Then, most tourism was focused on popular places, such as Halong Bay. We realised the potential of these (less-visited) destinations and decided to create scheduled tours, which were very popular.”

In 2011, Trinh launched PYS Travel, and organised private tours to more off-the-beaten-track spots that were geared mainly towards the domestic market, with some international arrivals.

Fast forward to 2016, Trinh noted a spike in demand for domestic travel. However, the booking process proved cumbersome, with tourists largely having to book transport, accommodation and activities separately.

Wanting to provide a one-stop online shop for domestic travellers while offering tourism players an additional platform to promote and sell their products, Trinh set about partnering with airlines and hotels to create Tago.vn, a subsidiary of PYS Travel. The company was launched in 2017, offering tourists a variety of options for holiday packages that included flights and accommodation.

Trinh said: “Tago.vn was born to help people make their holidays easier and happier. We wanted to provide a one-stop-shop solution for customers, so they can book and enjoy trips easily, which encourages more travelling. (Using the platform) is convenient, time-saving and gives customers better prices than booking each service separately.”

The average trip length for Vietnamese holidaymakers is four days, as compared to seven nights for other Asia-Pacific countries, according to a Visa Global Travel Intentions report.

Since its launch, Tago’s customer base has grown from 9,500 annually to more than 12,000 in 2018, putting it on track to hit nearly 18,000 this year, and expand to over 34,000 by 2021.

Gross merchandise value has also increased from US$1.2 million in 2017 to US$2.2 million last year. This is estimated to reach US$3.8 million this year, and grow to more than US$7.5 million by 2021.

Having secured partnerships with hospitality giants, including Vinpearl, FLC Hotels & Resorts, as well as Accor and Flamingo, Trinh said that Tago offers companies an easy and additional avenue to sell their products.

He added: “For suppliers, like hotels, they have more channels to sell. As Tago sells packages instead of just hotel rooms, the prices are hidden so hoteliers can (decrease) prices during the low season without creating any conflict with other selling channels.”

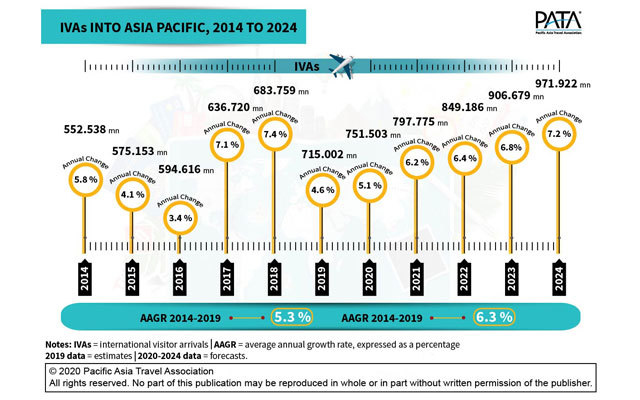

Asia-Pacific remains solidly on the path to welcome close to one billion international visitor arrivals (IVAs) over the next five years. This was one of the key predictions from the Executive Summary of the Asia Pacific Visitor Forecasts 2020-2024, released yesterday by the Pacific Asia Travel Association (PATA). Covering the years 2019 to 2024 and 39 destinations within the region, these forecasts anticipate a volume of over 971 million international visitor arrivals into Asia-Pacific, by 2024.

The strong increase in IVAs has been driven by the average annual growth rate (AAGR) of 5.3% between 2014 and 2019, and that momentum is expected to increase even further over the next five years, to average 6.3% per annum between 2019 and 2024.

This will result in an acceleration of more than 256 million additional IVAs into the region between 2019 and 2024, a significant increase over the additional volume of 162 million added between 2014 and 2019.

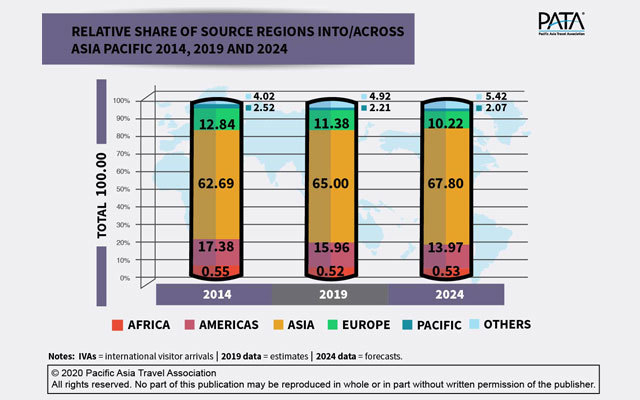

The distribution of these IVAs in Asia-Pacific is expected to change only marginally from 2019, with the Asia and Pacific regions expected to show some relative, as well as absolute increases in arrival numbers.

Asia is forecast to remain as the dominant destination region and is likely to improve its relative share to over 77% by 2024. The Americas will come in second, although its share is expected to reduce slightly over the period between 2019 and 2024.

As a generator of IVAs into and across Asia-Pacific however, Asia is predicted to continue growing in relative share, accounting for almost 68% of all IVAs into the region in 2024. This is likely to be at the expense of both the Americas and Europe, both of which are predicted to wane, at least in terms of their respective shares as source regions for Asia-Pacific, between 2014 and 2024.

Eleven Asia-Pacific destinations are predicted to each receive more than 10 million additional IVAs between 2019 and 2024, with China leading the way, expecting to add around 38.2 million more arrivals to its inbound count and raising the aggregate volume to almost 208 million in 2024.

Japan is ranked next, followed by Macau, China and then Mexico, with all of these destinations expected to receive more than 20 million additional foreign arrivals each, over the forecast period to 2024.

The top group of 11 destinations, as shown in Exhibit 4, is likely to account for 77% of the IVA volume into Asia-Pacific in 2024 and more than three-quarters of the additional arrivals over that same period.

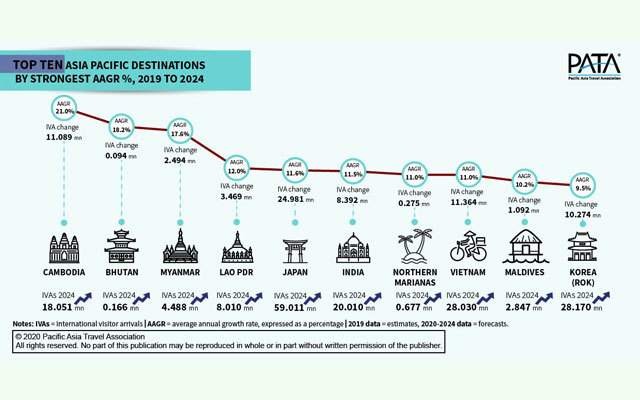

In addition, it is predicted that nine out of 10 destinations will have AAGRs between 2019 and 2024 in excess of 10%, ranging from 10.2% for the Maldives to 21% for Cambodia. The volume bases for each of these destinations vary widely, however these very strong average rates of growth are certainly worth closely watching over the forecast period.

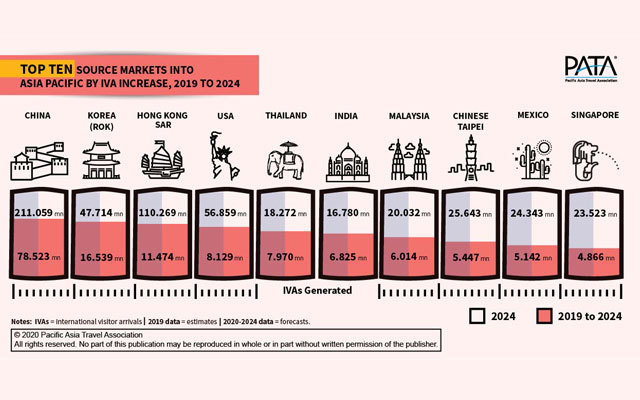

The top 10 strongest source markets into Asia-Pacific between 2019 and 2024 are forecast to include China, the Republic of Korea and Hong Kong SAR in the top three positions, generating a collective volume of more than 369 million IVAs over that period. These three source markets alone are also predicted to generate an additional volume of more than 106 million IVAs into Asia-Pacific over the same period.

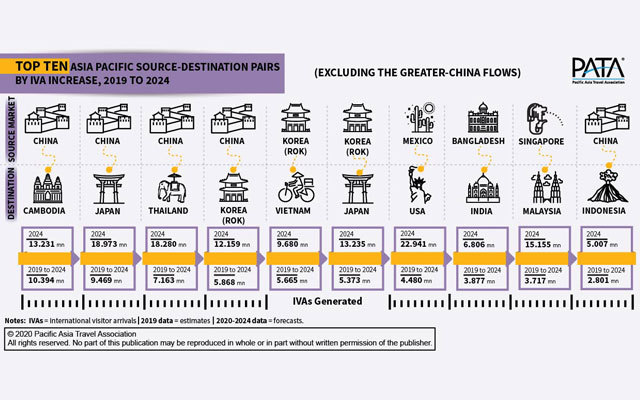

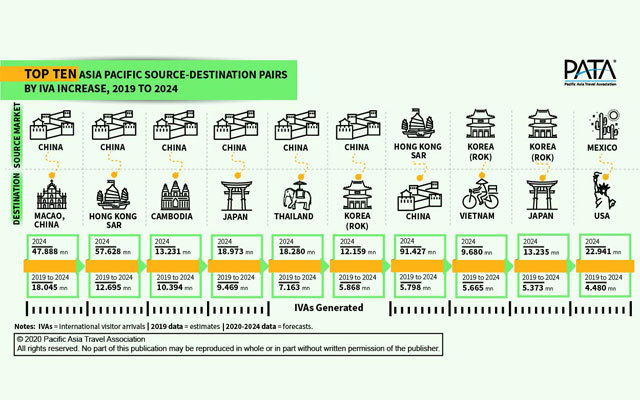

Much of that volume is, of course, generated by internal Greater China flows, especially from China into Macau, China and Hong Kong SAR and to a lesser degree vice-versa as can be seen from the top source-destination pairs as shown in Exhibit 7.

Adjusting for the Greater China source-destination pairs, the importance of China for a number of other Asia Pacific destinations becomes obvious, with China appearing five out of the possible ten times, as a major source market.

The relative strength of the close intra-regional flows also becomes evident in the top ten cluster of source-destination pairs as illustrated in Exhibit 8.

PATA CEO’s Mario Hardy commented on these forecasts: “For many destinations, there is now an immediate and necessary shift from generating arrivals to properly managing those visitors. It is no longer enough to think and talk about this, the time to put into action such management practices that ensure that visitors into and across the Asia Pacific region receive a superlative and memorable experience is now.”

“The tourism juggernaut is a reality, and this means that, as a socio-economic sector, travel and tourism needs to ensure that it has the necessary mindset and infrastructure – both hard and soft – to enable the growth of this magnitude to be properly managed. It is incumbent upon us all to deliver both memorable experiences and positive outcomes for visitors, residents and the environment in equal measure.”

Key mainland China hotel markets are projected to report performance growth in 2020 despite a challenging macroeconomic environment, according to the latest forecast from STR and Tourism Economics.

“China’s economy, and by extension its hospitality industry, remains strong, even with concerns around the trade war with the US and an overall global economic slowdown,” said Christine Liu, STR’s regional manager, North Asia.

Beijing Daxing International Airport is the second international airport of Beijing

“A decline in Chinese departures to other countries, combined with significant government investment in infrastructure is driving domestic demand in key markets. However, the country’s resiliency to difficult macroeconomic situations will be tested if the trade war continues to decelerate economic growth.”

At the market level, Beijing should continue on its growth trajectory with a forecasted increase of 3.7% in revenue per available room (RevPAR). Average daily rate (ADR) is expected to continue to grow (+1.8%) after a strong 2019 in the metric.

“Demand growth is key for Beijing as supply continues to increase at a healthy rate. The newly opened Beijing Daxing International Airport, projected to be one of the busiest in the world; and Beijing preparing for the 2022 Winter Olympics, highlight potential growth for the tourism and hospitality sector,” Liu said.

After a challenging 2019, Chengdu is forecasted for ADR growth of 1.4%. The market is projected to report the country’s second-largest supply growth rate (2.8%) with close to 18,000 rooms in the development pipeline. Demand will be helped by China’s high-speed train system and subsequent MICE business.

As the international trading centre and comprehensive transportation hub of China, Guangzhou is expected to show RevPAR growth of 3.4% with solid increases in both occupancy and ADR.

Hangzhou, known for welcoming a mix of leisure and business travellers, is set to see its run of performance growth end in 2020 (RevPAR: -2.4%). Among key markets in mainland China, Hangzhou should see the largest increases in supply (+4.1%) and demand (+4.7%).

Following three years of occupancy declines owing to new supply, 2020 is expected to be Shanghai’s year of recovery. RevPAR growth is expected to reach 2.5% as the market is likely to pick up displaced demand caused by continued protests in Hong Kong.

To further attract the Indian outbound MICE market, the Penang Convention & Exhibition Bureau has rolled out a specialist programme, as well as introduced a new support package, as part of a roadshow to India.

The Penang Specialist Programme will be a full-day workshop and Indian stakeholders with first-hand knowledge of Penang. The certification is valid for three years upon which qualifying members will be invited for recertification.

Penang sellers meeting with Indian buyers during the roadshow

Among the incentives that the Penang Specialists can qualify for are incentives for group sales of 100 pax and above, fam trips to Penang, opportunities to attend PCEB’s training and networking programme in Penang and India, and more.

A new support package specially tailored for the Indian market has also been rolled out. Support packages start from as low as sponsorship of souvenirs and welcome luncheon for the organisers valued at RM3,500 (US$858; for confirmed meetings/conferences of 50 to 100 delegates) to hosted site inspections, welcome luncheon for organisers, cultural performances and souvenirs valued at RM10,000 (for incentive groups of 501 delegates and above.)

These announcements and activities were part of the Penang Roadshow to India 2020, led by Penang’s minister for tourism Yeoh Soon Hin and CEO of PCEB Ashwin Gunasekeran, and supported by a delegation of 14 hotel, attraction, and DMC partners.

The roadshow began in Mumbai on January 13, and the team was in New Delhi on January 15. Next up are Chennai on January 17 and Kochi on January 20. In each city, there will be a B2B engagement session with Indian MICE stakeholders, as well as a media session with local Indian and MICE media.

“The number of Indian travellers to Penang has also increased in recent years. The Penang Immigration Department reported that for the period between Jan to Dec 2019, 61,847 Indian travellers visited via the Penang International Airport and Penang Swettenham Port (cruise liners) compared to 43,537 in the same period in 2018. This is a 42 per cent increase, making it one of the healthiest growths we have experienced,” revealed Gunasekeran.

“India is one of the top five markets for business events in Penang, and over the past years, we have received encouraging interest from event planners and conference organisers. In 2019, four per cent of business events of Asia-Pacific origin was from India, contributing RM268.6 million (US$65.9 million in estimated economic impact,” he added.

Data and analytics will continue to be one of the key drivers of the commercial aviation industry going into a new decade, predicted travel data and analytics expert Cirium, but it warned that analytics will have to become much more human-centric, with a significant focus on end-users.

David White, director, market development at Cirium, said: “The past decade’s biggest challenge for commercial aviation has been to safely keep up with a rate of passenger demand that is straining the systems’ capacity. The skies are crowded, the competition is fierce, and operational environment is extremely complex. Airlines and airports have had to get much smarter about how to use technology, data, and process to squeeze additional capacity out of limited resources.”

Aviation industry leverage big data analytics to facilitate predictions and forecast demand, but there needs to be greater focus on end-users: Cirium

Here are the top 5 aviation and travel trends to watch in 2020 and beyond, according to Cirium’s industry experts:

Human-centered data and analytics 2.0

While big data and analytics became popularised in the previous decade, there is still a lot of untapped potential. The race to extract meaningful and valuable information out of new data sources has only just begun.

Steve Wilson, data scientist at Cirium, said: “The amount of data being generated by aircraft, locations and devices is increasing. Getting this data wrangled and into decision makers should help make the industry more efficient. This mountain of data being created – something like 100 billion GB annually as estimated by Oliver Wyman – can be used for forecasting and predictions. Deep learning models, despite not being quite capable of general artificial intelligence, should prove really useful in reaching gains and improvements for the industry.”

If you think of data-driven intelligence as a series of phases, then 2020 will herald the human-centered phase of our data evolution. The previous phase was about using structured and unstructured data to answer questions after an event. The next phase will be a matter of anticipating behaviour and providing answers before questions need to be asked.

Predictive maintenance

Quality data is the foundation for any type of predictive capability. Now that the technology needed to collect, process, prepare and structure massive amounts of device data exists, there is a good chance machine learning could evolve enough in the next decade to monitor patterns and events in real-time.

“There is already a focus on data collection and analytics to drive aftermarket service revenue growth for aircraft manufacturers, MRO service providers and systems suppliers,” said Andrew Doyle, director, market development at Cirium.

“The next step is development and deployment of predictive maintenance algorithms enabling replacement of critical components prior to failure, leading to a significant reduction in aircraft technical delays.”

Airline revenue management

The power of predictive analytics doesn’t stop at the physical parts of an aircraft. Airlines and airports are getting better at predicting consumer demand and optimising price or inventory to maximise revenue growth. For example, airlines now have tools at their disposal to accurately forecast demand on a cabin level, thereby getting a look at their true profit in a market.

“If you look at the US domestic market, both American and Delta have come out with growth plans that are above the industry three to four per cent growth rates,” said Nathan Greer, sales engineer at Cirium. “Delta is managing this by upgrading to larger aircraft, while American is doing the same, in addition to reconfiguring aircraft with additional seats.”

Accommodating predicted demand isn’t something airlines will be able to do alone. It will take collaboration and connection across the industry to achieve new levels of revenue growth.

“Certain Asian markets are the fastest growing in the industry. The challenge for the 2020s will be to expand the ability of airlines, airports, and ANSPs to share data and collaborate across the region in order to keep traffic flowing, passengers safe, and to deliver a quality service. Tokyo’s 2020 Olympics will be a good test for the overall network,” White said.

A current barrier to increased collaboration among airlines and airports is the reluctance to share data. Trust and ownerships of data remain major issues in the industry. However, the key to making progress in maximising revenue in 2020 and beyond will be a less restricted exchange of data. The benefits of this exchange will mean a more seamless journey towards developing more sophisticated, enhanced analytics.

“In the decade to come, I think we can expect to see technology largely improving airline and airport operational efficiency,” said Joanna Lu, head of consultancy, Asia, at Cirium. “Data and information sharing among stakeholders in the industry shall be improved to face the headwinds.”

Dynamic personalisation

It’s widely known people buy experiences, not products. In the decade to come, each part of the trip experience will be impacted through personalisation powered by machine learning – from in-flight services to pre-trip planning and disruption recovery.

While the 2010s were an era for change in the way customer problems were addressed, the 2020s will be a time where brands get smarter about every single customer touchpoint. The next logical step after customer service is customer engagement. It’s no longer sufficient to quickly answer questions and resolve problems. The time has come to create ongoing interactions between customer and company, shaped by the customer profile.

“Airlines are stepping up their game to adapt and engage individual traveller types by analysing their preferences, behaviour and demographics,” said Charles Brossman, senior product manager at Cirium. “They’re launching new and exciting customer engagement strategies to interact with them. This makes customers feel noticed and appreciated, which is critical to building brand loyalty.”

Tailoring messages and services to individual travellers is the expectation right now, particularly among Millennials. Yet, most airlines and other travel service providers still don’t have the right mix of data, technology and people to achieve a personalised experience customers will remember. The opportunity to impress and win over travellers on an emotional level is still wide open.

Cirium’s marketing director Carrie Mamantov said: “Automated personalisation will finally be coming to travel. A few airlines are getting all their data organised and breaking down the siloes to better link up the different dimensions of customer information. Look for loyalty to build with the brands who can predict needs and behaviour based on the omni-channel experience finally becoming more actionable.”

Providers across the industry will endeavour to link their value to traveller data. From manufacturing to tech services, every part of the ecosystem has an opportunity to be valuable to airlines and travellers.

Eco-consciousness

The travel industry has been one of the major targets of environmental criticism in recent years. Air travel accounts for about 2.5 per cent of global carbon dioxide emissions, after all.

Airlines are already having to take stronger action to minimise their carbon footprint. In this new decade, they will also be expected to ensure fuel efficiency isn’t outstripped by growing demand.

“We are seeing the very early stage of electric aircraft now flying in Canada,” said Alistair Rivers, director, market development at Cirium. “There will be pressure to reduce operations of current fuel-operated aircraft. I live in hope of a coordinated single European sky from an air traffic control point of view as this has massive potential to save both fuel and time by allowing aircraft to fly more directly.”

Preliminary traffic figures for the month of November 2019 released by the Association of Asia Pacific Airlines (AAPA) showed international air passenger markets recorded a further increase in demand, stimulated by the availability of affordable airfares and improvements to connectivity.

In aggregate, the region’s airlines flew 30.3 million international passengers in November, a 3.4 per cent increase compared to the same month last year. The moderate growth reflects the general slowdown in global economic activity.

International air passenger markets are still growing at a constant clip

International passenger load factor averaged 80.1 per cent for the month, after accounting for a 3.6 per cent increase in demand as measured in revenue passenger kilometres (RPK) and a 2.6 per cent growth in available seat capacity.

Commenting on the results, Andrew Herdman, AAPA director general, said: “Asian airlines carried a combined 342 million international passengers during the first eleven months of the year, achieving 4.2 per cent growth despite falling business confidence levels and corresponding moderation in economic activity across regions. Tourism activity continued to lend support to leisure travel, with growth within the region boosted by the availability of affordable air fares.”

Looking ahead, Herdman said: “The outlook for air passenger markets is still reasonably positive, with expectations of continued moderate expansion in the global economy. Meanwhile, the region’s carriers remain vigilant in monitoring and responding to changes in market conditions, while seeking new growth opportunities.”