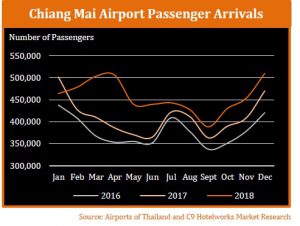

Medical tourism generates one-third or more of revenue for private hospitals in most South-east Asian countries, according to a new report by Zion Market Research, which found Asia-Pacific dominating the growing medical tourism market in 2017.

Zion Market Research projects that the global medical tourism market could generate revenue of around US$28 billion by the end of 2024, based on an estimated CAGR of around 8.8% from 2018.

In 2017, the global medical tourism market generated revenue of US$15.5 billion.

Asia-Pacific dominated the medical tourism market in 2017 with “significant revenue share”, Zion Market Research said in its new report.

Private hospitals generate major revenue from foreign patients. In most ASEAN countries, medical tourism represents one third or more revenue of a private hospital, according to the report.

In India, medical tourism accounted for 25% of revenue, and in Taiwan, the Philippines, and South Korea, approximately 10-15%.

In the region, public healthcare reforms are rapidly expanding the private sector, which is expected to drive medical tourism market growth.

Europe contributed to significant revenue share in 2017. The growth is attributed due to the increasing flow of patients, healthcare experts as well as advancement in medical technology in the region.

In particular, the report noted that people in Germany, Great Britain, and the Scandinavian countries use services provided in Polish medical institutions frequently.

However, it foresees that the lack of implementation of the European Directive on the application of patient’s rights in cross-border healthcare may impede industry growth.

In 2012, Passport2Health was the first health insurance plan launched in the UK based on medical tourism; it offers a private diagnosis for patients at home, private treatment overseas in Europe in the selected network hospitals, and follow-up care and rehabilitation in the UK. The policy was provided for small and medium-sized businesses and individuals

Latin America market is projected to experience lucrative growth during the forecast period. Market growth is particularly expected in Brazil and Mexico.

According to Zion, various companies are engaged in building and operating hospitals in Mexico that meet American standards, mostly for American and Mexican patients. Prices in Mexico is around 40% less than the US. Cash-paying, uninsured Americans have benefits for treatment procedures in Mexico, including price quotes and package prices.

Overall, Zion Market Research attributes medical-based migration to low-quality healthcare infrastructure and services and high treatment expenditure. Rising awareness level among people regarding advanced medical facilities are the foremost factors expected to drive medical tourism market growth over the forecast period.

Developing countries are increasingly focussing on technological advancement and quality services in the medical and healthcare sector.

However, the global market research firm said tourists are associated with a wide variety of health risks after they return.

Medical conditions include deep vein thrombosis, TB, amoebic dysentery, paratyphoid, and many others; caused due to poor post-operative care and inadequate rest.

Additionally, stringent documentation processes, visa approval issues, and inadequate insurance coverage are some of the factors which impede the growth of the medical tourism market.

Increasing investment in healthcare by various government and private sectors is anticipated to further drive industry growth.

At present, more than 700 hospitals and medical departments across the globe are accredited by Joint Commission International (JCI) in the US. The number of accredited facilities is projected to increase by 20% almost every year.

Based on treatment type, the medical tourism market is segmented into cancer treatment, orthopaedic treatment, fertility treatment, cardiovascular treatment, neurological treatment, and others.

The report includes profiles of end players such as Fortis Healthcare, Bumrungrad Hospital Public, Bangkok Dusit Medical Services, Asian Heart Institute, Prince Court General Hospital, Apollo Hospitals Enterprise Limited, KPJ Healthcare Berhad, Samitivej Sukhumvit, Spire Healthcare, Medanta, Min-Sheng General Hospital, IHH Healthcare Berhad, Raffles Medical Group, and others.

“Despite the large number of expatriates living in Australia from these countries, their long-lasting appeal to tourists and affordable flights have also made them ever-popular choice for travellers in Australia.”

“Despite the large number of expatriates living in Australia from these countries, their long-lasting appeal to tourists and affordable flights have also made them ever-popular choice for travellers in Australia.”